Introduction to Investing

Through investing, you can build wealth for a strong financial future. Defining your goals and creating and sticking to a plan by regularly setting money aside for investments can drive life-changing results over time.

- What is Investing?

- Compound Growth

- Managing Risk

- Asset Allocation and Diversification

- Long-Term Investments

- Savings and Short-Term Investments

- Investing for Your Children

- Other Steps to Build Wealth Over Time

What is Investing?

Both saving and investing mean you're setting aside some of the money you earn, separate from what you spend on needs and wants. A savings account is a good choice for short-term goals or to hold an emergency fund that can cover unexpected expenses. You can open a savings account at a bank or credit union, and the money you deposit there is typically federally insured. Most banks or credit unions will pay some interest on your savings.

Investing is when you put your money into assets such as stocks or bonds, often held in a brokerage or advisory account, with the expectation of making a return over time. Return from an asset may come from an increase in the asset’s value or from an asset’s interest or dividend payments to those who own it.

All investments involve risk and you should allow for market fluctuations over time. You can invest in different types of products.

Investing doesn’t have a set rate of return, but some experts consider a 7 – 10% annual rate of return as a useful estimate for long-term diversified investments in US stocks, based on historic averages.

Compound Growth

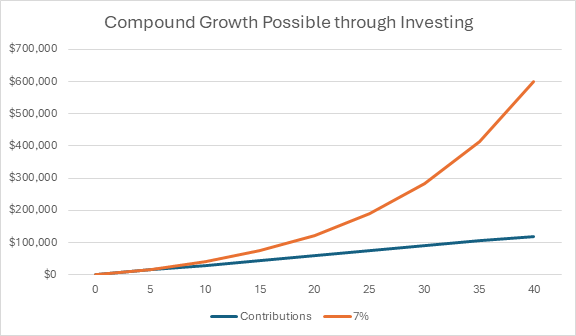

Compound growth happens when you earn a return on money you invest as well as on the return your invested money earns. When you invest over a period of years and keep those funds invested, you benefit from this compound growth, which is like a snowball rolling on the ground and picking up additional snow with each rotation.

The graph below shows the power of compound growth. If you set aside $100 each month for 40 years, that money has the potential to grow over time through the power of compound growth. This graph assumes a 7% average annual rate of return.

With long-term investing, the formula is: regular investments + time → wealth. Determine your time horizon by choosing the amount of time you dedicate to reaching your goal. If you start investing early in your career for a long-term goal like retirement, your time horizon is considered long-term because you will not use those funds for decades. Knowing your time horizon will help you develop your investing goals.

Regular investing means that you put a set dollar amount or a set percentage of your income into your investment accounts. The earlier you start investing, the more powerful the impact of compounding becomes. Your snowball rolls down the hill more times, gathering more snow.

It’s never too late to get started, but starting later means you will need to invest more of your earnings to reach your goals. When possible, take advantage of salary increases by increasing the amount of your regular investment contribution and you’ll increase your overall wealth.

The examples below show how much you would need to invest each month to hit a goal of $500,000 or $1 million, assuming a 7% average annual rate of return.

| Age You Start Investing | $500,000 by Age 65 | $1,000,000 by Age 65 |

| Age 18 | $127/month | $254/month |

| Age 25 | $209/month | $418/month |

| Age 35 | $441/month | $883/month |

| Age 45 | $1,016/month | $2,033/month |

| Age 55 | $3,016/month | $6,032/month |

Managing Risk

All investments have some degree of risk. Markets fluctuate over time, and individual investments may lose value. But there are steps you can take to help minimize the risk of investing.

Knowing your time horizon and your personal tolerance for risk is helpful. If you’re investing for a retirement that is 30 years away, you have time to manage market fluctuations. If you prefer to be more conservative with your money, that’s good to know. These factors will help you choose the types of investment products that are right for you.

Asset Allocation and Diversification

Two important strategies for managing investing risk are asset allocation and diversification.

Asset allocation involves dividing your investments among different “asset classes”, such as stocks, bonds, and cash. Finding the right mix for you will involve assessing your risk tolerance and your time horizon.

Diversification is summed up by the phrase, “don’t put all your eggs in one basket.” One way to diversify is to distribute your investments among different kinds of assets. The idea is that if one investment loses money, other investments may make up for some of those losses.

You could buy shares of a single company, but then your financial performance will depend exclusively on how that single company’s stock performs. Numerous factors can impact a stock’s price including the effectiveness of company management, product strength, consumer demand, economic changes, labor and supply chain costs, or even the changing preferences of your fellow investors.

Another option is to invest in companies, securities, or investment products that are built to provide exposure to a broader cross section of the market. An index fund is a product that seeks to track a market index, which measures the performance of a “basket” of stocks and bonds and is representative of a stock market or an economy.

Diversification can help reduce your losses if the market drops, because when different sectors may be down, other sectors may rally and allow a diversified investor to break even or even post gains. Some products are structured to provide diversification, like target date funds.

Long-Term Investments

If you are a long-term investor, you are investing for goals many years in the future like a college education or retirement. When it comes to retirement, many long-term investors take advantage of investing accounts offered by their employer, which typically provide tax advantages and other benefits.

A workplace retirement plan, like a 401(k) or a 403(b) or 457(b) is a benefit of many jobs. Contributing to one may reduce the amount of taxes you pay. Many employers match contributions you make up to a certain amount. Consider contributing at least that amount so you can take full advantage of your employer’s matching funds so you don’t lose out on that free money.

Another type of retirement saving account is one that you set up yourself, known as an Individual Retirement Account or IRA. You can invest in your own tax-advantaged investment account to provide financial security when you retire. IRA contributions can also reduce the amount you pay in taxes.

You can invest in both an employer provided plan and an IRA, but there are limits to how much you can contribute each year. Once you contribute to a retirement-focused investment account, you will have options for how you want to invest the contribution you and your employer have made.

Many people choose to invest their contributions in a mutual fund or exchange-traded fund (ETF). Target date funds in these accounts may automatically shift toward a more conservative mix of investments as you approach your anticipated retirement date.

For many investors, workplace retirement savings programs and IRAs are the foundational building blocks of their investment portfolio, and a critical part of their overall financial plan.

Other types of long-term investment accounts include Education Savings plans known as 529 Plans, ABLE Accounts for those with qualified disability expenses, Health Savings Accounts (HSAs), and Trump Accounts.

Savings and Short-Term Investments

Some goals require use of your money in the not-too-distant future, like buying a car, a near-term down payment on a house, or the start-up costs for a small business. In those situations, you may be seeking investments with less potential risk and volatility such as money market funds, certificates of deposit (CDs) or investment grade bonds.

Funds for short-term goals are generally held in an account that allows you to access the funds quickly without any tax penalties or significant fees. Some examples of these accounts include high-yield savings accounts or brokerage or advisory accounts.

Investor.gov has information on other investment products, including their common attributes and risks.

Investing for Children

- Trump Accounts (530A) – Launching on July 4, 2026, Trump Accounts are tax-advantaged investment accounts that can be opened for U.S. citizens under age 18. The account is held in the child’s name, with a parent or guardian serving as custodian until the child reaches age 18.

- 529 College Savings Accounts - A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education costs. 529 plans, legally known as “qualified tuition plans,” are sponsored by states, state agencies, or educational institutions and are authorized by Section 529 of the Internal Revenue Code.

- Custodial IRAs - Children can have IRA accounts if they have earned income. Parents can open these accounts as custodial accounts.

Other Steps to Build Wealth Over Time

While investing regularly over a long period of time can be an important part of a wealth building plan, there are other steps that can boost your chances to grow your net worth.

- Make a Plan or Budget - Start by listing your income, expenses, savings and investment contributions. Prioritize long-term saving and investing goals by setting up automatic contributions to those, while making sure your income covers your monthly living expenses. Live within your means.

- Pay Down High Interest Debt - If you have high interest credit card debt, consider taking steps to pay off that debt aggressively and limit your use of credit cards. If you don’t pay off that balance every month, you’ll be paying interest charges that may greatly exceed the amount you could earn on your savings or investments.

- Build An Emergency Fund - Many investors use their bank or credit union to set aside some “rainy day” funds so that they don’t have to go into debt if they have an unexpected expense, like a car repair.

- Protect Your Investments - Scammers use a variety of techniques to convince investors to hand over their hard-earned money. Learning the tactics scammers use and how to spot the red flags of investment fraud will help you keep your money safe.

For most Americans, a retirement savings plan, which you build over time during your working years, is an essential part of securing your retirement. Learn what you can do, while employed and once retired, to make the most of your investments.